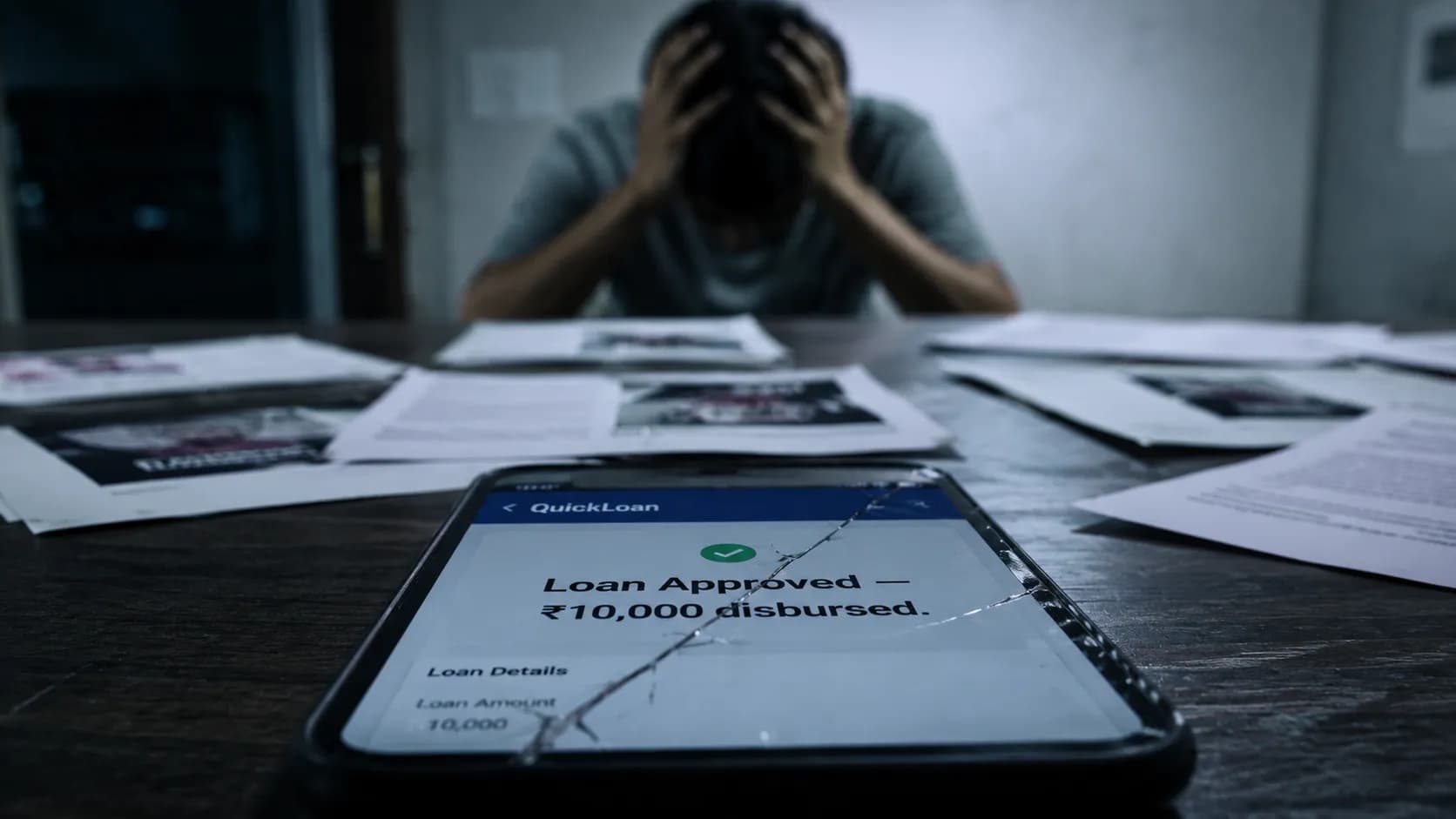

The trap closes the moment you accept. The ₹5,000 disbursement is real, but your contacts, photos, and peace of mind now belong to them.

The ad promises instant approval. No documents. No credit score check. ₹5,000 in your account within minutes. You download the app. You fill in your details. You tap "Allow" on a few permission requests without reading them. The money arrives.

Three days later, the first message comes. They have your contacts. They have your photos. They have sent a morphed image to your sister, your boss, or your neighbour, and they will send more unless you pay. The ₹5,000 loan has become a ₹50,000 extortion.

This is not an edge case. In December 2025 alone, the Indian government blocked 87 illegal loan apps operating exactly like this. Thousands more are active right now, with new names and new Play Store listings uploaded within hours of each takedown. The technology is cheap. The victims are everywhere. And the law has a clear answer for what these apps are doing and what you should do before you install anything.

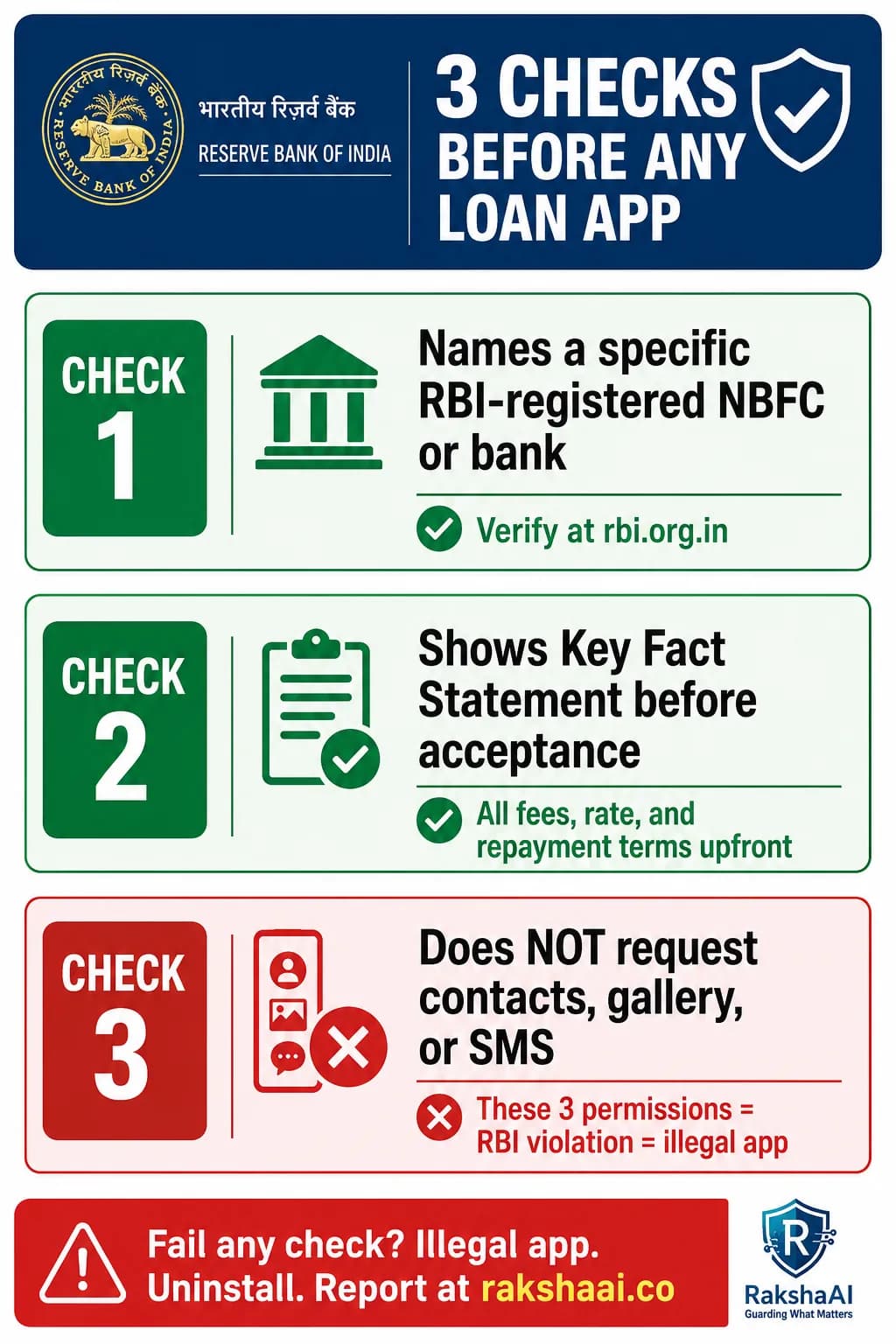

3 RBI checks to identify a fake loan app in India

- 1Must clearly name a specific RBI-registered NBFC or bank as lending partner

- 2Must show a Key Fact Statement (KFS) before you accept the loan

- 3Must NOT request access to your contacts, gallery, or SMS messages

These permissions are explicitly banned by RBI Digital Lending Guidelines. Any app failing these 3 checks is illegal. Uninstall immediately.

What Are Fake Loan Apps? The Real Purpose

A fake loan app is not primarily a lending business. It is a data extraction operationdressed in the clothing of a fintech company. The loan is real: a small disbursement to establish credibility and trigger your consent to continue. The real product is the data your phone hands over the moment you tap "Allow."

Unlike legitimate digital lenders (which are registered NBFCs or banks with RBI oversight), illegal loan apps are typically operated by shell companies with no traceable Indian registration. Many route money through mule accounts. Some are operated from networks in Southeast Asia with Indian-speaking call centre staff handling the harassment phase.

The economics are simple: one successful blackmail victim can generate ten times the original loan amount. The app costs almost nothing to build. The Play Store listing is uploaded under a new name every time one is taken down. It is an industrial-scale extortion machine that uses your own contacts as the weapon against you.

How a Fake Loan App Traps You: Phase by Phase

Phase 1: The Attractive Entry

The entry point is always engineered to remove hesitation. The app appears in search results for queries like "instant loan no documents India" or "same day personal loan." It has a polished interface, a recognisable-sounding name ("QuickCash", "RupeeLoan", "LoanBuddy"), and often hundreds of fake five-star reviews uploaded in bulk.

The offer is calibrated to catch people at their most vulnerable: ₹2,000–₹10,000, instant approval, no CIBIL score required, no branch visit. For someone facing an emergency: a medical bill, a missed salary, a rent due tomorrow. This is exactly what they are searching for.

Phase 2: The Permission Grab

This is where the actual crime happens, and it happens before a single rupee changes hands. During registration, the app requests access to:

- Contacts: your entire address book

- Gallery and Photos: every image on your phone

- SMS messages: your OTPs, bank alerts, personal messages

- Sometimes: Camera and Microphone

Most users tap through these permissions without reading them. The app frames them as "required for KYC verification" or "needed to assess creditworthiness." None of this is true. RBI's Digital Lending Guidelines explicitly ban loan apps from accessing contacts, gallery, and SMS. Any app that asks for these three permissions is, by definition, non-compliant with Indian law.

The moment you grant access, your data is uploaded to remote servers. The loan amount is trivial compared to the value of that data as a blackmail instrument.

Phase 3: The Small Disbursement

The app disburses the loan, often less than what was advertised, with unexplained "processing fees" deducted upfront. You receive ₹3,500 when you applied for ₹5,000. The repayment schedule begins almost immediately, sometimes within seven days, at interest rates that translate to 300–400% annualised, a level that is illegal under RBI guidelines.

This phase serves two purposes: it confirms you have an active bank account (useful for future fraud), and it establishes the debt that will be used to justify the harassment that follows.

Phase 4: The Harassment and Blackmail

When repayment is due, or sometimes even before, the harassment begins. Recovery agents call you, your family members, your colleagues, and your employer. They use your contacts list to identify who matters most to you. They send morphed images combining your photos with compromising content to your WhatsApp contacts.

The messages are designed to produce maximum shame and urgency: "We have notified your family", "Your colleagues have been informed of your defaulter status", "Pay immediately or we file a police case." None of this is legal. All of it is a crime under India's IT Act, the RBI's lending guidelines, and the Indian Penal Code.

For many victims, the shame drives them to pay repeatedly, far beyond the original loan amount, rather than face the social consequences of the morphed images being shared more widely. This is exactly what the operators are counting on.

The 3 RBI Checks to Do Before Any Loan App

The Reserve Bank of India's Digital Lending Guidelines give you three objective tests that separate legal lenders from illegal operators. They take under two minutes and require no technical knowledge.

Share this card with anyone who might be considering a loan app. These 3 checks take 2 minutes and can prevent total financial and personal devastation.

Check 1: Does the app name a specific RBI-registered NBFC or bank?

Every legal digital lender must clearly disclose its registered lending partner: a specific NBFC or bank whose name you can verify at rbi.org.in. Vague descriptions like "licensed by financial authorities" or no mention of a lending partner at all are disqualifying. If you cannot find the named NBFC in the RBI registry within two minutes, the app is illegal.

Check 2: Does the app show a Key Fact Statement before you accept?

RBI requires all digital lenders to show a Key Fact Statement (KFS), a standardised document listing the exact interest rate, all fees, the total repayment amount, and the grievance redressal mechanism, before you agree to the loan. If you are being asked to accept a loan without seeing a KFS first, the lender is non-compliant.

Check 3: Is the app asking for contacts, gallery, or SMS?

This is the most important check and the easiest to verify. Before you install any loan app, check what permissions it requests on the Play Store or App Store listing. If contacts, gallery/photos, or SMS appear in the permissions list, stop. Do not install. These three permissions are explicitly prohibited under RBI's Digital Lending Guidelines for loan apps. Any app requesting them is operating outside the law.

All three checks pass? Still verify the NBFC name on rbi.org.in before you proceed. A legitimate lender will never pressure you to skip this step.

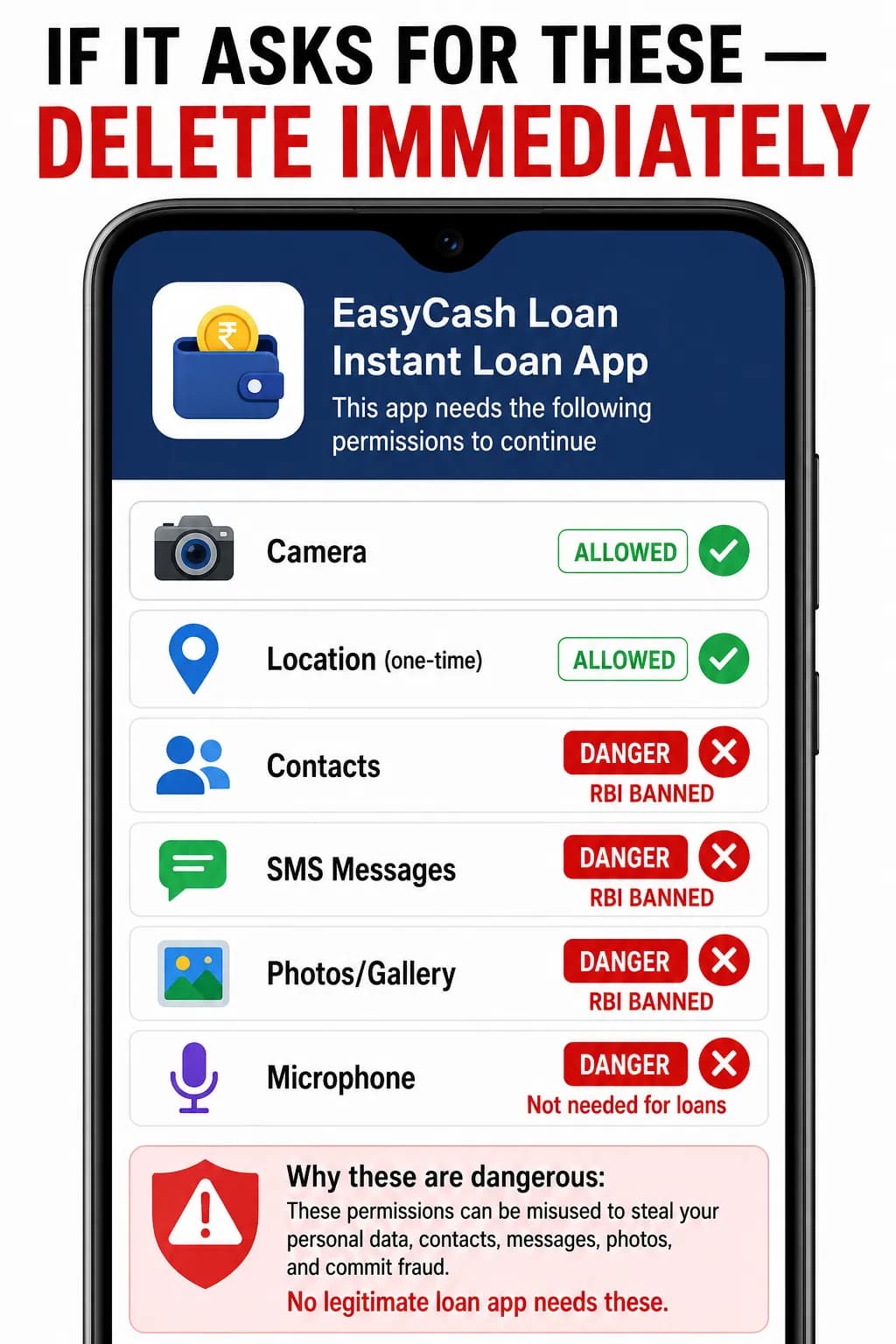

Permission Red Flags: What a Loan App Can and Cannot Ask For

If a loan app requests contacts, SMS, or gallery, it is violating RBI guidelines. Deny all permissions and uninstall immediately.

Understanding what permissions are legal versus illegal takes the guesswork out of evaluating any loan app.

Permissions a legitimate loan app may request:

- Camera: for selfie-based KYC identity verification

- Location: one-time, for address verification

- Storage: limited, for uploading documents only

Permissions that are RBI-banned for loan apps:

- Contacts: no legitimate lender needs your address book

- SMS Messages: no legitimate lender needs to read your messages

- Gallery/Photos: no legitimate lender needs your photo library

- Microphone: not needed for any lending function

The reason illegal apps want contacts and photos is not creditworthiness assessment. It is to create a hostage situation. Your contacts become the threat, and your photos become the weapon.

What To Do If You Are Already Being Harassed

Stop all payments immediately. Every payment you make extends the blackmail. It proves the tactic works and makes you a target for further demands. Payment is never the solution.

Save this plan. If you or someone you know is being harassed by a fake loan app, these 6 steps are the correct response, in this order.

- Stop all payments immediately. Payment is not a solution: it is a confirmation that the extortion works. Operators know that paying once means you will pay again. Every rupee you send funds another round of harassment.

- Warn your contacts via WhatsApp. Send a message to your address book explaining that your number has been compromised by a loan app scam and that any disturbing images or messages they receive are fake. This neutralises the weapon before it is used.

- File an FIR at your local cybercrime police station. Bring screenshots of all conversations, the app name, the UPI ID or bank account used, and copies of every threatening message. A formal FIR is required for any legal action.

- File at cybercrime.gov.in. The National Cybercrime Reporting Portal creates a digital record that supports police investigation and can trigger coordinated action across states.

- Report to RBI Sachet at sachet.rbi.org.in. Filing with the RBI creates a regulatory record. The Sachet portal specifically tracks illegal lending operations and has been used to initiate app takedowns.

- Report the app on RakshaAI. Your report flags the number and app for other Indians who may encounter the same operator before they become the next victim.

A Note on Shame: This Is Not Your Fault

The most effective weapon these operators have is not technology. It is shame. The design of the harassment is specifically calibrated to make you feel that reporting will cause more damage than paying. That is a lie, and it is the lie that keeps the entire operation profitable.

People who have been targeted by fake loan app blackmail are not careless or foolish. They were targeted by a system that is specifically engineered to be invisible until it is too late, with permissions buried in onboarding flows, morphed images created from genuine photos, and social pressure applied through relationships you actually value.

Thousands of Indians face exactly this situation every month. Reporting does not increase the shame: it increases the chance that the operators are stopped before they do this to someone else.

If you are in psychological distress from this experience, please call:

Mental Health Support (24/7, free)

iCall: 9152987821 | Vandrevala Foundation: 1860-2662-345

Frequently Asked Questions

How do I check if a loan app is registered with RBI India?

Visit rbi.org.in and search for the NBFC name displayed in the app. All legal digital lenders must disclose their registered lending partner. Also check the RBI Sachet portal at sachet.rbi.org.in for alerts about illegal lending apps operating in India.

What should I do if a fake loan app is blackmailing me?

Stop all payments immediately. Payment extends the blackmail. Warn your contacts via WhatsApp, file an FIR at your local cybercrime station, file at cybercrime.gov.in, and report to RBI Sachet. Mental health support: iCall 9152987821 (24/7, free).

Can a loan app legally access my contacts or photos in India?

No. RBI's Digital Lending Guidelines explicitly prohibit loan apps from accessing contacts, gallery, or SMS. Any app requesting these three permissions is non-compliant and almost certainly predatory. Deny all permissions and uninstall immediately.

How many fake loan apps have been banned in India?

In December 2025 alone, 87 illegal loan apps were blocked under India's IT Act. Thousands more have been blocked in previous crackdowns. New fake apps constantly appear under different names. Always check the 3 RBI criteria before installing any loan app.

What is the RBI Sachet portal for fake loan app complaints?

RBI Sachet at sachet.rbi.org.in is the Reserve Bank of India's portal for reporting unauthorized digital lending. Filing creates a regulatory record that supports police investigations and can trigger RBI action against illegal operators.

Final Thoughts

The fake loan app trap works because it is designed around genuine need and genuine trust. People who download these apps are not doing anything unusual. They are trying to solve a real financial problem using a tool that looks exactly like a legitimate solution.

The protection is three questions asked before you install. Does the app name a specific RBI-registered NBFC? Does it show a Key Fact Statement before you accept? Does it avoid requesting contacts, gallery, and SMS? If any answer is no, walk away. No emergency is worth the alternative.

If you have already been targeted, you are not alone and you are not at fault. Report, warn your contacts, and get support. The operators rely on silence to continue. Your report here or at cybercrime.gov.in, and that is the one thing that actually stops them.

Free Tool

Got a suspicious loan app or number?

Check any phone number, app name, or website on RakshaAI instantly. No sign-up. No cost. Results in under 5 seconds.

Check a Number or App now →100% free · No sign-up required · Save 1930 in your contacts

More from RakshaAI Blog

Stay Protected Online

Use RakshaAI to check websites, phone numbers, and UPI IDs for scams free, instant, no sign-up required.

RakshaAI is a private platform by Ehatech Services Pvt. Ltd. Not affiliated with any government body. Editorial policy